First Home Super Saver Scheme (FHSS): 2026 Guide

First Home Super Saver Scheme: How to Use Your Super for a First Home Deposit

On this page ▾

- What is the First Home Super Saver Scheme (FHSS)?

- Is the First Home Super Saver Scheme worth it?

- Who is eligible for the FHSS scheme?

- How much can you withdraw under FHSS?

- How the FHSS scheme works, step by step

- How to apply, and the timing that trips buyers up

- Tax on FHSS contributions and withdrawals

- FHSS vs other first-home-buyer schemes (and how to combine them)

- How FHSS fits into your deposit and home loan

- Frequently asked questions

- Final word

The First Home Super Saver Scheme (FHSS, sometimes written FHSSS) lets you save for your first home deposit inside your super, then withdraw those savings when you’re ready to buy. Because money inside super is taxed at a lower rate than money in a regular savings account, the scheme can help most first home buyers build a deposit faster. FHSS contribution limits, caps and tax figures in this guide are current for the 2025-26 financial year, sourced from the ATO.

Here’s the part the bank explainers tend to skip: FHSS is only useful once you connect it to the actual purchase. The money you release becomes part of the deposit on your first home buyer loan, it lowers how much you need to borrow, and the timing of the release has to line up with your contract and settlement. This guide covers the scheme itself, then shows how the released money fits into your deposit and your home loan.

What is the First Home Super Saver Scheme (FHSS)?

The FHSS scheme is a federal government program that lets first home buyers make extra voluntary contributions into super, then withdraw most of those contributions (plus deemed earnings) to put toward a first home deposit. You cannot touch your compulsory employer super or your existing balance. Only the voluntary contributions you choose to make on top count.

It works because of tax. Salary-sacrifice contributions are taxed at 15% going into super, which is usually well below your marginal income tax rate. So the same dollar of pre-tax income builds a bigger deposit inside super than it would after tax in a normal bank account. The ATO sets out the full rules on its First Home Super Saver Scheme page, and the government summarises the scheme on firsthomebuyers.gov.au.

FHSS is federal, so the rules are the same whether you’re buying in Sydney, Brisbane, Perth or anywhere else in Australia. State first home buyer concessions vary, but FHSS does not.

Is the First Home Super Saver Scheme worth it?

For most first home buyers who can afford to make voluntary contributions, yes. The tax treatment means you reach your deposit target faster than saving the same money outside super, and because the money sits in super, it’s harder to dip into than cash in an everyday account. But it isn’t right for everyone, and the benefit depends heavily on your income and your timeline.

Pros

- Tax saving inside super. Salary-sacrifice contributions are taxed at 15% instead of your marginal rate. On a 32.5% or 37% marginal rate, that gap is real money kept in your deposit.

- Harder to raid. Super isn’t a tap-and-go account, so the deposit builds instead of leaking out to other spending.

- Deemed earnings on top. You don’t just get your contributions back. The ATO adds an associated earnings amount, so the released figure is larger than what you put in.

- Per-person access. Couples can each use the scheme on the same property, which roughly doubles what the scheme can contribute to a joint deposit.

Cons and who it doesn’t suit

- If your marginal tax rate is already low, the gap between the 15% super rate and your normal rate is small, so the benefit shrinks for lower earners.

- Your money is locked in super until release. You can only access it through the FHSS process and only to buy a first home. It isn’t an emergency fund.

- It rewards planning, not last-minute buyers. FHSS suits people with a 1 to 3 year runway to contribute. If you’re buying next month, there’s little time for the scheme to do its work.

What are the risks of using FHSS?

The scheme is low-risk by design, because your savings sit in super and the released earnings are a fixed deemed amount rather than a market return. The real risks are procedural, and they’re avoidable once you know them.

- Contribution-cap traps. Your FHSS contributions count toward your normal super contribution caps. Go over the cap and the excess isn’t FHSS-eligible. We cover the cap maths below.

- Timing mistakes. Request your determination too late, and you can lose eligibility. This is the single most common trip-up, so we’ve given it its own section.

- The deal falls through. If you’ve released the money and don’t buy within the allowed window, you either recontribute it or pay a 20% tax. Manageable, but worth planning around.

- Reduced flexibility. Once contributed, that money is committed to the FHSS pathway. If your plans change and you decide not to buy, getting it back out has tax consequences.

Who is eligible for the FHSS scheme?

To use FHSS, you must meet all of the following:

- Be 18 or older when you request your FHSS determination. You can make eligible contributions before you turn 18, but you have to be at least 18 to request the determination that releases them.

- Have never owned property in Australia. That includes an investment property, vacant land, commercial property, a lease of land, or a company-title interest. A limited financial hardship exception applies (see below).

- Have never previously requested an FHSS release. It’s a one-time scheme per person.

- Intend to live in the home. You need to genuinely intend to move in as soon as practicable and live there for at least 6 of the first 12 months. It has to be a home you’ll occupy, not an investment, and your name must be on the title.

You don’t need to be an Australian citizen or permanent resident to use FHSS, which sets it apart from some other first home buyer schemes. The financial-hardship exception is narrow: the ATO can determine that you lost all your previous property interests through an event like bankruptcy, relationship breakdown, loss of employment, serious illness or a natural disaster, in which case prior ownership doesn’t automatically rule you out.

Eligibility is assessed per person. Couples, siblings or friends buying the same property can each use their own FHSS savings. And if one partner has owned a home before, that doesn’t stop the other eligible partner from applying.

How much can you withdraw under FHSS?

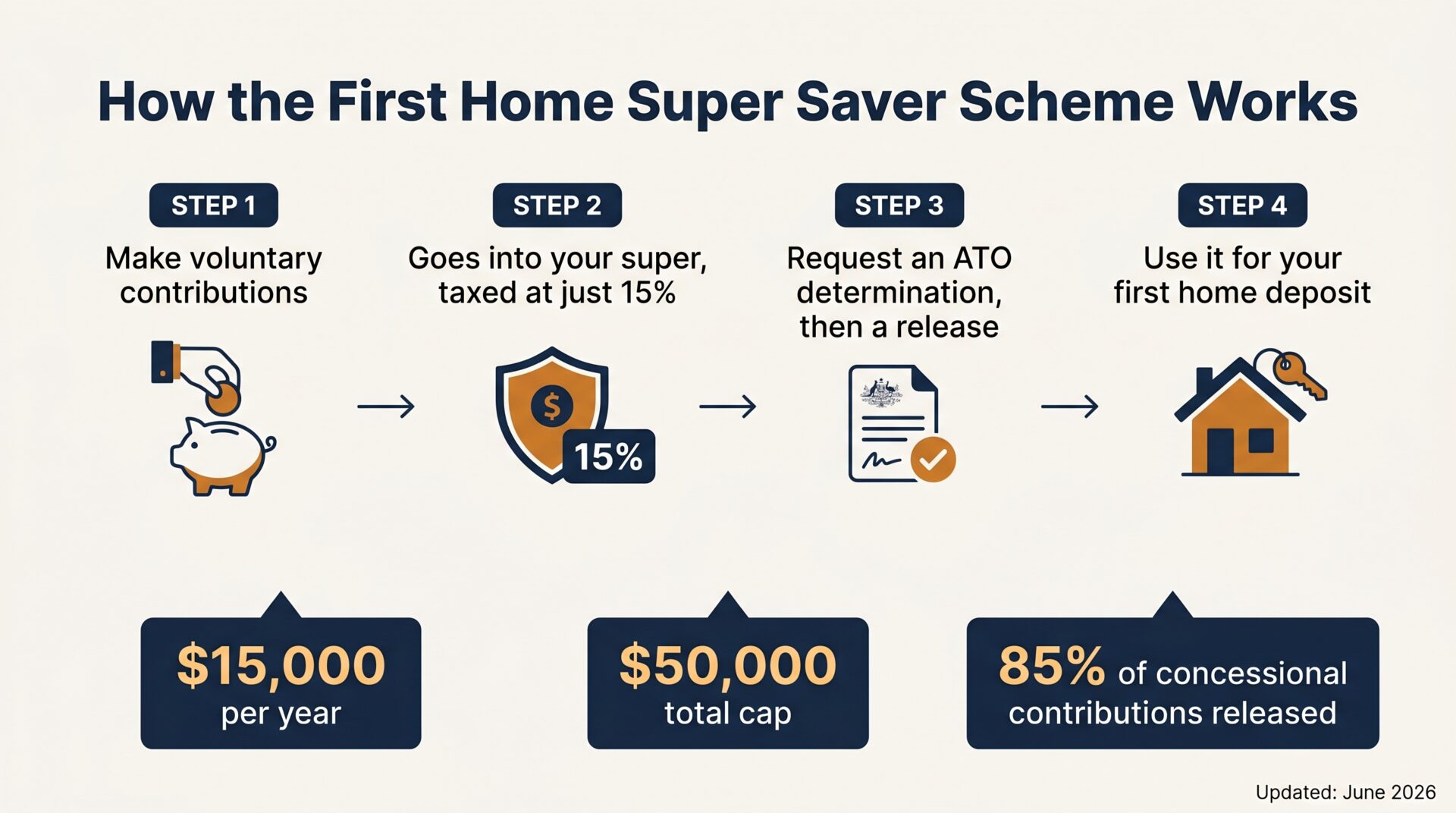

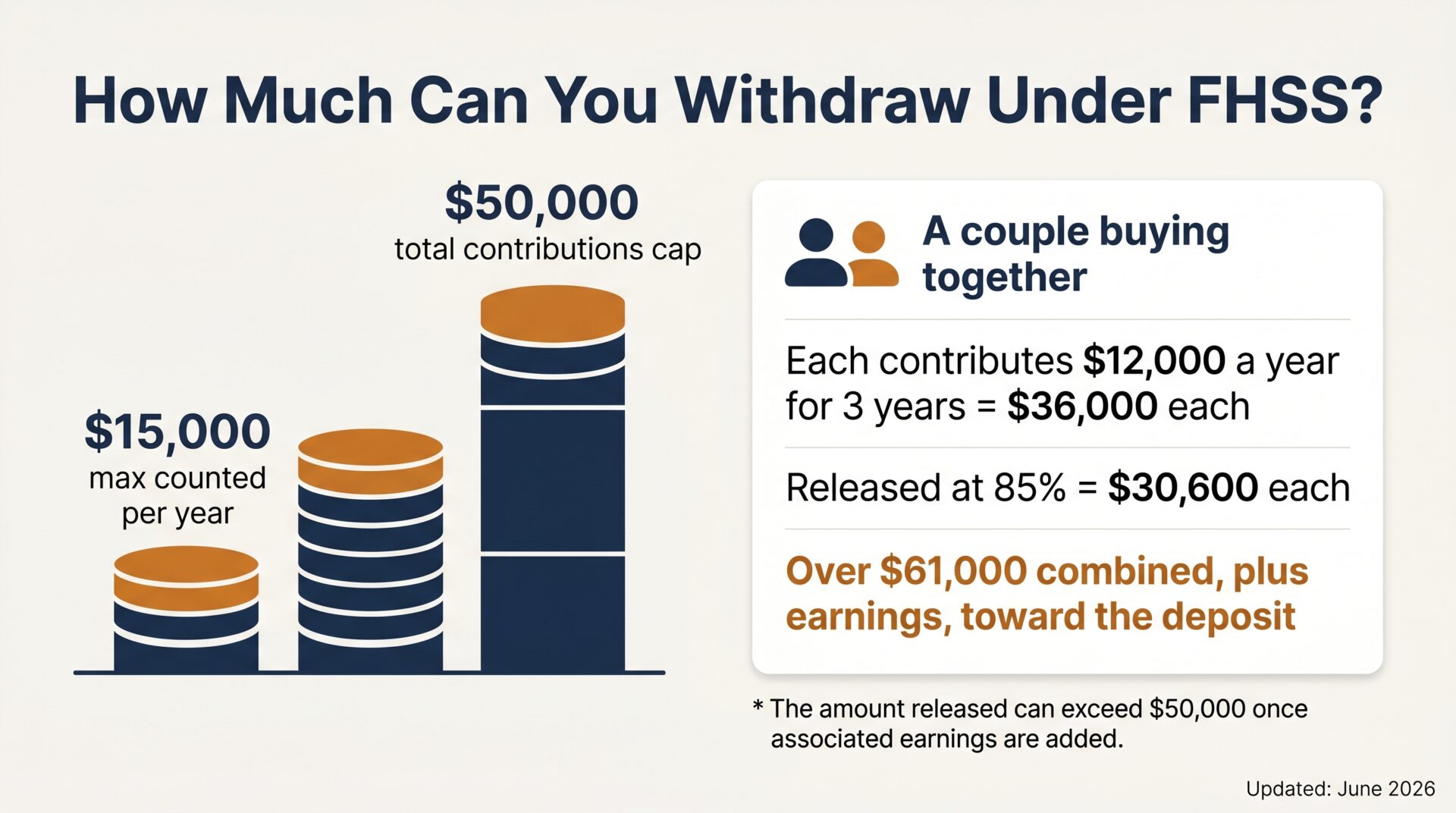

You can have a maximum of $15,000 of eligible voluntary contributions counted per financial year, up to a total of $50,000 of contributions counted across all years (for contributions made from 1 July 2017). Those limits apply to your full voluntary contributions first. The releasable proportions are then applied on top:

| What you can release | Proportion |

|---|---|

| Eligible personal contributions you did NOT claim as a tax deduction (non-concessional) | 100% |

| Salary-sacrifice contributions (concessional) | 85% |

| Personal contributions you DID claim as a deduction (concessional) | 85% |

| Associated (deemed) earnings on the above | Added on top |

Concessional contributions are released at 85% because they were already taxed 15% going into super, and that 15% stays in the fund. Two points that catch people out:

The $50,000 is a cap on the contributions counted, not on the cash you get back. Associated earnings are added on top, so the amount actually released can be higher than $50,000.

The limits apply before the 85%/100% split. The ATO’s own worked example makes this clear: if you salary-sacrifice $25,000 in a single year, only $15,000 counts as an eligible FHSS contribution that year, and only 85% of that ($12,750) counts toward your releasable amount.

One thing to clear up: FHSS is not the COVID-era $10,000 super early-release scheme. That was a separate, now-closed program for financial hardship. FHSS has no $10,000 cap, and you can only ever release your own voluntary contributions, never your compulsory employer super.

A worked example for a couple

Say Jordan and Sam are buying their first home together. Each salary-sacrifices $12,000 a year for three years, so each has $36,000 of eligible concessional contributions (comfortably under the $15,000-a-year and $50,000-total limits). At 85%, that’s $30,600 each that’s releasable, plus associated earnings. Between them, that’s over $61,000 of contributions plus earnings going toward the deposit, instead of the same money sitting in an after-tax savings account earning a fully taxed return.

Associated earnings are a deemed figure, not your fund’s actual return. The ATO calculates them at the shortfall interest charge (SIC) rate, which is the 90-day Bank Accepted Bill rate plus 3%, compounded daily and updated every quarter. For the July to September 2026 quarter, that rate is 7.43%, but because it moves each quarter, you should treat any single figure as a snapshot. You can check the current rate on the ATO’s shortfall interest charge rates page.

To model your own numbers, the ATO’s FHSS estimator inside myGov is the authoritative tool. Our home loan calculators can then help you turn a deposit figure into a borrowing target and an estimated repayment.

How the FHSS scheme works, step by step

- Make voluntary contributions to your super through salary sacrifice or personal contributions, staying within the $15,000-a-year and $50,000-total FHSS limits and your normal contribution caps.

- Request an FHSS determination through myGov (ATO online services). The ATO calculates and tells you your maximum release amount.

- Request a release. You get one release request, so choose your amount (up to the determination maximum), your fund and your bank account carefully.

- Sign your contract to buy or build, and notify the ATO within 90 days of signing.

- Receive your money. The ATO says it usually takes 15 to 20 business days for your fund to release the money and for the ATO to pay it (less withholding tax) to your bank account.

How to apply, and the timing that trips buyers up

This is where FHSS goes wrong for people, and it’s the part that super fund explainers gloss over. The order of operations matters.

Get your determination before ownership transfers to you. The hard legal rule is that you must request your FHSS determination before ownership of the property passes to you, which in practice means well before settlement. Leave it until you’ve settled and you’ve missed the window.

You do not have to request the release before you sign a contract. This is a common misconception. For determinations made on or after 15 September 2024, you can request your release before signing a contract, or within 90 days after signing. Signing a contract first does not automatically blow your eligibility, provided you got the determination in time and request the release within that 90-day window.

Build the 15 to 20 business day release time into your plan. The FHSS money isn’t sitting in your bank account the day you sign. That has a practical consequence: your FHSS funds usually aren’t available as your deposit-at-exchange (the deposit you hand over when you sign). They form part of the money you bring to the settlement instead. If you need cash at exchange before your FHSS release lands, a deposit bond can bridge that gap.

You then have 12 months to sign a contract, which the ATO can extend automatically to a maximum of 24 months without you applying. Miss that, and you either recontribute the assessable amount as a non-concessional contribution, or keep the money and pay FHSS tax of 20% on the assessable released amount.

This is exactly the kind of sequencing a broker handles with you, so your release, your contract and your settlement line up.

Tax on FHSS contributions and withdrawals

FHSS is taxed in two places: going in and coming out.

Going in, concessional contributions (salary sacrifice, or personal contributions you claim as a deduction) are taxed at 15% inside super. That’s the saving. Compared with paying tax at a marginal rate of 32.5%, 37% or higher on the same income, the 15% rate leaves more of your money working toward the deposit.

Coming out, the ATO works out your assessable FHSS released amount, which is the concessional contributions plus the associated earnings on everything. That assessable amount is included in your income for the year you request the release, and it’s taxed at your marginal rate (including the Medicare levy), less a 30% tax offset. In practice, the ATO withholds tax at your expected marginal rate less 30%, or a flat 17% if it can’t estimate your rate, then squares it up when you lodge your return. Your non-concessional contributions (the personal contributions you didn’t claim a deduction on) are not taxed again on the way out, because they were paid from money you’d already been taxed on.

For most first home buyers, the net tax outcome works in your favour, but if you’re a high earner, get advice on how the offset interacts with your marginal rate before you commit.

FHSS vs other first-home-buyer schemes (and how to combine them)

FHSS is a deposit-building tool. The other big first home buyer measures are deposit-reducing tools, which is why they work together rather than competing.

| Option | What it does | Best for |

|---|---|---|

| First Home Super Saver Scheme | Helps you save a bigger deposit inside super at a lower tax rate | Buyers with a 1 to 3 year savings runway who want to grow the deposit |

| Australian Government 5% Deposit Scheme | Lets eligible first home buyers borrow up to 95% without paying LMI | Buyers with a small deposit who want to buy sooner |

| Guarantor home loan | A family member’s equity covers part of your security, reducing or removing the deposit need | Buyers whose parents can help with security |

| Saving outside super | A normal savings account or term deposit | Buyers who need the money fully accessible and flexible |

The key point: you can stack these. FHSS builds your deposit, and the Australian Government 5% Deposit Scheme reduces how much deposit you need in the first place. Use your FHSS savings as part of the deposit on a 95% loan, and you’ve attacked the problem from both ends. A guarantor home loan is another lever you can combine with FHSS if family support is available.

How FHSS fits into your deposit and home loan

This is the bit that turns FHSS from a super technicality into a home you actually buy.

Every extra dollar of deposit lowers your loan-to-value ratio (LVR), which is your loan amount as a percentage of the property value. A lower LVR means a smaller loan, a stronger application, and often a sharper interest rate. Most importantly, it affects lenders mortgage insurance (LMI): LMI normally applies when you borrow above 80% LVR, and the premium climbs as your LVR rises toward 95%. If your FHSS release lifts your deposit across an LMI pricing threshold, the drop in premium can run to thousands. If you want the mechanics, our guide to what LVR means and how it’s calculated walks through it.

If FHSS alone won’t get you to your deposit target, that’s normal, and it’s where the loan side comes in. A 95% home loan lets eligible buyers purchase with a 5% deposit plus costs, and a no deposit home loan backed by a guarantor can close the gap entirely. FHSS makes whichever path you choose cheaper, because it shrinks the slice of the purchase you’re borrowing.

The question that follows is usually “how much income do I need to borrow the rest?” That depends on your deposit, your expenses and current lending buffers. Run the deposit figure through our home loan calculators for a first estimate, then we can model it properly against real lender policies.

Frequently asked questions

Can I use the FHSS scheme if I have owned property before?

Generally no. You must never have owned property in Australia, which includes an investment property, vacant land, commercial property or a company-title interest. There’s one narrow exception: the ATO can grant a financial-hardship determination if you previously lost all your property interests through events like bankruptcy, relationship breakdown, illness or natural disaster. And if a couple buys together and one of you has owned before, that doesn’t stop the other eligible partner from using FHSS.

Can I combine FHSS with the Australian Government 5% Deposit Scheme?

Yes. They do different jobs and stack neatly. FHSS helps you build a bigger deposit by saving inside super at a lower tax rate, while the 5% Deposit Scheme lets eligible first home buyers borrow up to 95% of the property value without paying lenders mortgage insurance. You can use your FHSS savings as part of the deposit you bring to a 5% Deposit Scheme loan.

What if my purchase falls through?

You have 12 months from your release request to sign a contract to buy or build, and the ATO can extend this to a maximum of 24 months automatically. If you still haven’t signed by then, you either recontribute the assessable amount back into super as a non-concessional contribution, or you keep the money and pay FHSS tax of 20% on the assessable released amount.

Can my partner and I both use the FHSS scheme?

Yes. FHSS eligibility is assessed per person, so two people buying the same home can each access their own contributions up to their own $50,000 limit, plus their own associated earnings. A couple can therefore put a materially larger combined deposit together than one person using FHSS alone.

When was the First Home Super Saver Scheme introduced?

It was announced in the 2017-18 Federal Budget and has been operational since 1 July 2017. Only voluntary contributions made on or after 1 July 2017 count toward your FHSS release amount.

What happens to contributions I don’t withdraw?

They stay in your super as normal retirement savings. You’re not forced to release everything. Any eligible voluntary contributions you leave behind keep earning inside super and stay preserved until you meet a standard condition of release, the same as any other super contribution.

One trap to plan around: your contribution caps

FHSS voluntary concessional contributions count toward your normal concessional contributions cap, which is $30,000 for the 2025-26 financial year. That cap already includes your employer’s compulsory super (12% in 2025-26), so on a decent salary you may have less room for $15,000 of salary sacrifice than you’d expect. Non-concessional contributions count toward a separate $120,000 cap. Check your headroom on the ATO’s contributions caps page before you max out, because contributions over the cap aren’t FHSS-eligible.

Final word

The First Home Super Saver Scheme is one of the few first home buyer measures that puts more deposit in your pocket rather than just lowering the bar to borrow. For buyers with a year or more to plan, the tax savings are genuine, and the per-person rules make it especially powerful for couples. The catch is the process: get the determination in before ownership transfers, request the release inside the 90-day window, and build the 15 to 20 business day release time into your settlement plan.

Where it gets valuable is when FHSS connects to the loan. Your released savings lower your LVR, can reduce or remove LMI, and stack with the 5% Deposit Scheme or a guarantor to get you over the line. If you’re working out how FHSS fits your deposit and what you can borrow on top of it, book a home loan assessment and we’ll map the whole picture, from your super release to settlement.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).